Are you planning a new office location, looking to optimize your space, or searching for a high-performing logistics or industrial site? Are you interested in profitable real estate investments? As a owner-managed real estate consulting firm, NAI apollo is here to assist you every step of the way. We support you with transactions, valuations, and asset management – regionally anchored and internationally networked.

Discover the cosmos of real estate

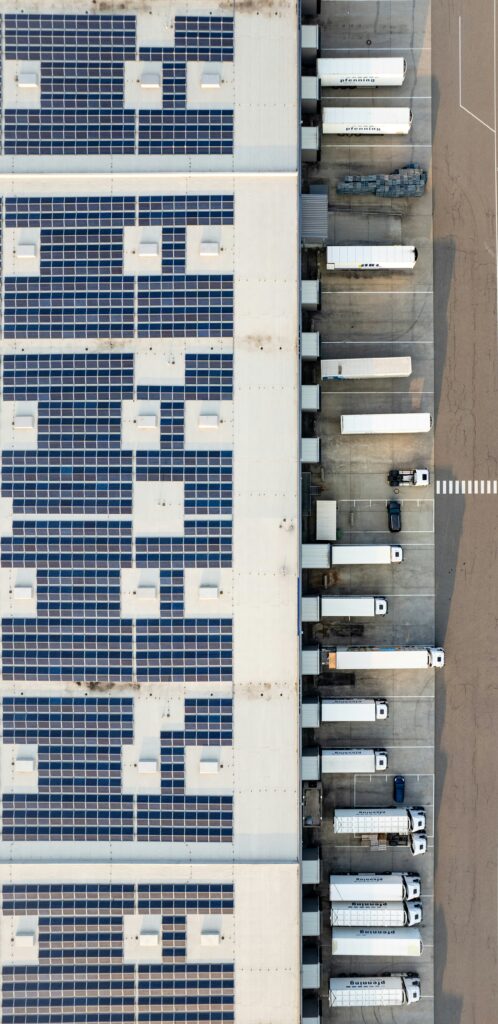

Highlights of our portfolio.

From financing and real estate management to rentals: benefit from our core services that cover the entire real estate cycle and create measurable added value for every target group: precise, efficient, and future-oriented.

Since our founding, NAI apollo has followed a clear goal

Creating sustainable value and achieving measurable results – for our clients and the market. With foresight and precision, we consistently set our course for the future of the real estate market – data-driven, dynamic, and visionary.

Success is measurable. And competence, experience, and a network of experts always lead to successful decisions. Benefit from international and national expertise with NAI apollo.

When competence meets passion

Bundled expertise for every type of real estate: Our leaders are not only masters of their craft, but visionaries who make your goals their mission.